Tax Increment Financing (TIF)

Overview:

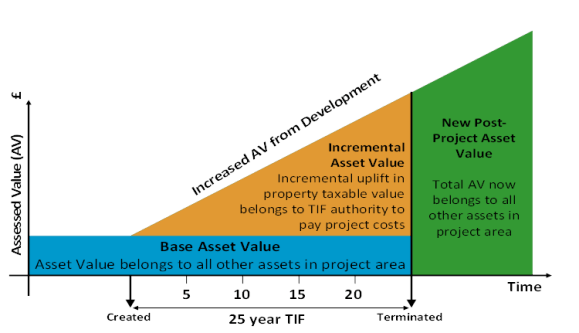

TIF is a complex and often misunderstood incentive. In the illustration below, the value of the property is on a trend to decline (or stagnate) over time absent of any intervention such as the use of TIF. Once a TIF Plan is in place, the property tax value is “frozen” while development takes place. Construction, that would have otherwise ceased to occur, is started and subsequently places the property on a more positive, long-term trend. The taxes associated with the increase value are captured to pay for the investment, but plenty of benefit to all taxing districts is realized in the prevention of further tax base erosion and additional tax base upon the termination of the district. For further explanation, please visit the following link outlining an example of effective TIF use.

Traditional Uses of TIF:

- -Redevelop areas with substandard buildings

- -Build housing for low-income and moderate-income families

- -Clean up pollution

- -Provide general economic development incentives

- -Finance public infrastructure, such as streets, sewer, water, sidewalks, and similar improvements

The Source of the Financing

TIF Districts capture the additional property taxes paid as a result of new development in the district to pay for part of the development costs. The tax revenue that is generated and collected on the new development is not distributed as provided in general law to the County, School District, City/Township and Special Taxing Districts, but instead is distributed to the TIF Authority that created the district. When a new building is constructed, the market value of the property and its property taxes typically rise. Classic examples would be building a new store on an undeveloped parcel or replacing one or more old buildings with a new, larger building. In both of these instances, the market value of the property will rise because the improvements add value to the parcel.

The “tax increment or increment” for the district is determined by multiplying the original tax rate by the captured retained net tax capacity. This roughly equals the taxes paid by the captured tax capacity or the increase in taxes that occur as a result of the development.